Should You Refinance Today?

There are a ton of factors that play into a refi decision — does it fit the business plan, would a sale be more attractive, should you just add a supplemental or two? And if you do decide to refi, then comes the haunting question: when is the best time to? Don't worry, we're here to help you quantify that decision point.

.png?width=544&name=Newsletter%20-%20On%20Tap%20(26).png)

To start analyzing a refi scenario, we'll pull the same sort of terms you'd expect: current financing economics, new financing assumptions, your prepayment penalty, and Treasurys or Forward Curves if applicable. But instead of stopping at a cashout number and saying "we can cash out big time, our investors are gonna love this!", we're going to take it a step further. Let's use an example...

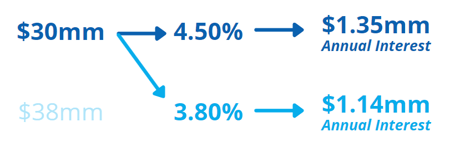

Say that these are the details of your existing financing:

- $30mm in outstanding principal

- 4.50% all-in fixed rate, locked on Treasurys + 1.80% at close

- Matures in two years

And then say these are the details of your new financing:

- $38m max proceeds

- 3.80% all-in fixed rate, locked on Treasurys + 1.80% (the 10T is at 2.00% as of writing this)

- 10 year loan term

Given a $1.35mm prepayment penalty and 1% closing costs, you'll cashout at $6.2mm in this scenario if you refi today.

Net Cost to Refinance

Ok, so what's the extra step?

As you already figure, the interest rate is a major component in a refi scenario - if spreads have tightened and rates are at 0, seems like a no brainer that there are interest savings there. Hence the wild popularity of refinances during 2020 and 2021.

Given that there's a savings opportunity, you can offset your cost to prepay the current financing by that savings amount. But, you have to compare apples to apples. You can't compare $30mm at 4.50% to $38mm at 3.80% because guess what... The new financing will have only slightly higher interest payments, by about $100k annually. So what does that even mean?

That comparison may make sense at first, and it does at face value, but to illustrate the issue: let's go wild and say you qualify for $50mm in proceeds. Then what? It's disingenuous to say you lose on the interest side, because you're comparing apples to oranges. Who wouldn't want to lever up at a lower interest rate, regardless of the interest payment dollar value being higher?

So, comparing today's financing at the current rate vs today's financing at the new rate (yes you read that correctly), we can get a more accurate picture of the interest savings.

That's the delta we can use to offset the prepayment penalty, and with that, you get a true net cost to refinance.

So let's say the prepay is Yield Maintenance and call it a back of the envelope $1.35mm penalty. With annual interest savings of $210k year 1 and $420k through the current financing maturity date, that $1.35mm can be considered offset by $420k. So your net cost to refinance is $930k.

Now, most people are with us up to here, but that's where they stop the analysis. So let's take it one more step further, what do you think?

Breakeven Analysis

Aka, what does that Net Cost translate to?

We break this part down into three steps, where we translate that dollar figure into rate movements.

Step 1. The Effect of 1 Basis Point on a New Financing. As rates move up or down by 0.01%, the Present Value of the new interest payments increases or decreases by the PV01. In this case, the PV01 for the new financing is appx $32k.

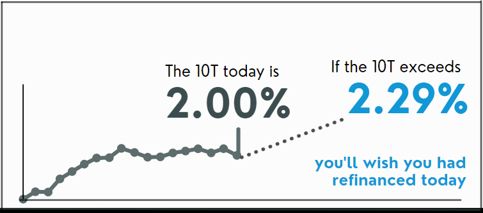

Step 2. Translate the Net Cost into the Rate. We can translate that Net Cost to Refinance into the rate on the new financing to determine how much rates need to increase before you should have refinanced when you had the chance. If the 10T goes bonkers and hits 20%, for instance, you'll really wish you had just paid the $930k to be locked into 3.80%.

In this scenario, the Net Cost and PV01 arrives at a +29bps max increase. Or, in other words, the fixed rate coupon would need to increase 0.29% in order to breakeven on upfront cost vs long term savings. If your all-in rate increases by more than that amount by the time you refi, you'll regret it.

Step 3. The Implied 10 Year Treasury Rate. Assuming no change in spreads, the implied 10T from this 29bp coupon increase gives us a 2.29% yield. If the 10T exceeds that, you'll wish you had refinanced today because your interest later will exceed your cost today.

What's the Likely Path of Rates?

If we knew what exactly is going to happen with interest rates, we'd be calling Garçon to bring over another mojito in the Bahamas right now instead of writing rate blogs. But alas we don't have a crystal ball, so all we can do is arm you with the math. From there, it's all about what you think is going to happen.

But to make it easier, we can refer to resources like this:

- Based on Implied 10T projections, which use average differences from the swap curve and the FOMC dot plot to interpolate, the 10T will be at 2.05% in two years, with a +1 standard deviation scenario putting it at 2.30%.

- Bloomberg's team of economists have on surveyed on average that they believe the 10T will hit 2.24% by the end of 2023.

- Goldman Sachs has raised it's 10T forecast to 2.25% by the end of 2022 and to 2.45% by the end of 2023.

- As you already know, volatility is all over the place, so it's especially tough to know what's going to happen. Odds that the 10T actually hits 20%?

Need help determining your breakeven point?

Feel free to reach out to support@loanboss.com, and we're happy to help!

Or check out our new refi analysis tools. They do the math for you!